Each year taxpayers have the opportunity to work with their tax preparer to craft a year-end tax plan that provides a desired tax liability. Taxpayers may use current tax legislation to lower or raise taxable income by claiming more or less taxable income during the current tax year. While working through tax planning decisions, taxpayers may wonder “What should my adjusted gross income be?” This article discusses adjusted gross income and identifiable signals which answer that question.

What is Adjusted Gross Income?

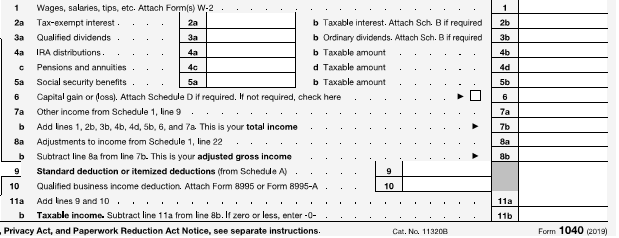

Individual income tax returns have changed a bit over the past several years; not only in how they appear to your eye but also the tax legislation that provides guidance as to their preparation. Some items remain constant. One of those is your Adjusted Gross Income (AGI). Let’s illustrate (Table 1) and discuss what is included in AGI.

Table 1: Excerpt of 2019 Form 1040

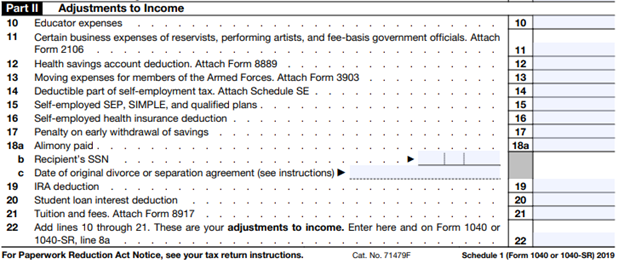

As illustrated above, AGI (Line 8b) is total income items minus adjustments. Items included in total income are wages, interest and dividends received, retirement distributions, social security benefits, capital gain (or loss), net business income and several additional qualifying income items that can be found in IRS 1040 and 1040-SR instructions (https://www.irs.gov/pub/irs-pdf/i1040gi.pdf). Please review the illustration below (Table 2) for a list of adjustments to income.

Table 2: Excerpt of 2019 Schedule 1

The adjustments listed above are subtracted from total income to arrive at adjusted gross income. Now that we know how to calculate AGI, let’s take a look at a few signals to help determine what AGI should be.

Calculation Example

AGI Signals

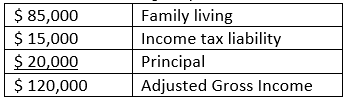

What a taxpayer’s AGI should be is a fairly straightforward calculation. AGI should be (at minimum) the sum of total amounts needed for family living expenses (medical expenses, groceries, personal bills), the prior year income tax liability and principal paid on loans. Please see the example below (Table 3).

$ 85,000 Family living

$ 15,000 Income tax liability

$ 20,000 Principal

$ 120,000 Adjusted Gross Income

To the extent that AGI is less than $120,000 (in the example above), tax deferral is generated. Tax deferral means a taxpayer moves taxable income to a future year by using tax strategies to generate a lower income tax liability in the current tax year.

Conclusion

Each taxpayer’s situation is different and varies from year to year. Use the examples and illustrations in this article (above) as a reference when considering year-end tax planning. Please work with your tax preparer to identify the best tax strategy for your current and future tax years.

About the Author: Jessie Shoopman

Shoopman is a field staff accountant at Illinois Farm Business Farm Management. She holds a master's degree in accounting from the University of Illinois - Springfield.

and then

and then