How often have you received your tax return back with a Schedule F for your farm operation that doesn’t reflect anything close to what you had expected? Did you think “I know I made more money than that?” or “Where did all that money go?” In this article we are going to explore the reasons why your cash basis and accrual farm income aren’t the same and why understanding the difference is extremely important when making management decisions.

What’s the Difference?

Let’s start with the differences in the cash and accrual accounting methods. Cash accounting is exactly that—your cash income and cash expenses in any given year. Many producers operate on and use cash accounting. In order to lower tax liabilities, producers may prepay input expenses or defer revenue. Accrual accounting looks to place your crop revenue and expenses in the proper year, which effectively removes those tax planning tactics (prepaying or deferring crop sales) for proper financial statement preparation.

Accrued Vs. Cash Example

Now that we have discussed these two accounting methods, let’s look at the tables below for examples to better illustrate how farm income can vary greatly from one approach to another.

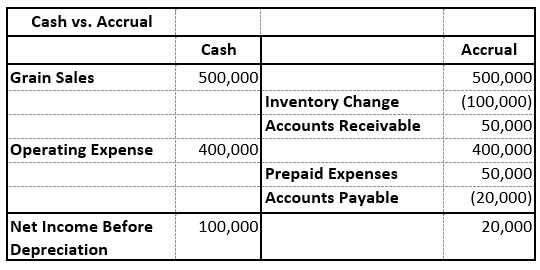

Table 1. Effect of a negative inventory change

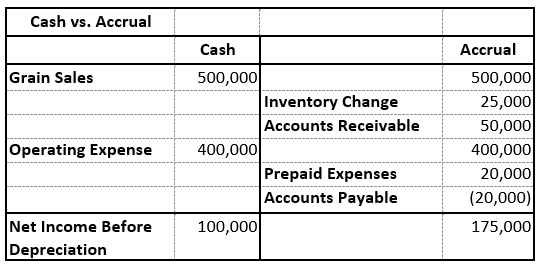

Table 2. Effect of a positive inventory change

As you can see (in Tables 1 and 2, above), once we’ve accounted for the change in inventory, accounts receivables, prepaid expenses and accounts payables, the accrued income is substantially different than cash income. Table 1 provides an example of decreased inventory value while Table 2 reflects an increase in inventory value. Inventory values can be affected by changes in bushels carried from one year to the next, changes in production and commodity prices. In the above examples, making a management decision purely based on the cash income position could cause potential challenges for the operation.

Historic Information

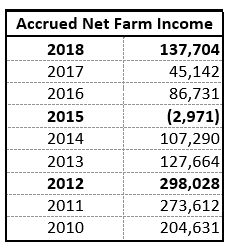

One of the best ways to learn is by looking at where we’ve been (in other words actual, historic results). The table to the right reflects accrual net farm income from Illinois FBFM farms.

You will note this table includes the highest EVER recorded accrued net farm income in Illinois FBFM’s financial database in 2012 and, just three years later, the lowest EVER recorded accrued net farm income. Looking at this historic data can help to identify years of unusual income and circumstances and provide a good benchmark to review.

Summary

Understanding the difference between your operation’s accrual versus cash income is extremely important. Using accrual adjustments, you can review a long-term outlook for your farm which allows for high level management decision making. Look to your farm’s historic results as a set of benchmarks and remember that incomes can vary tremendously from one year to the next, which is why it is so important to consider multiple years of data.

Reference

1Illinois FBFM 2018 Farm Business Results. Available at: www.fbfm.org

The author would like to acknowledge that data used in this study comes from the local Farm Business Farm Management (FBFM) Associations across the State of Illinois. Without their cooperation, information as comprehensive and accurate as this would not be available for educational purposes. FBFM, which consists of 5,500 plus farmers and 60 plus professional field staff, is a not-for-profit organization available to all farm operators in Illinois. FBFM field staff provide on-farm counsel with computerized recordkeeping, farm financial management, business entity planning and income tax management. For more information, please contact the State FBFM Office located at the University of Illinois Department of Agricultural and Consumer Economics at 217-333-8346 or visit the FBFM website at www.fbfm.org.

About the Author: Jessie Shoopman

Shoopman is a field staff accountant at Illinois Farm Business Farm Management. She holds a master's degree in accounting from the University of Illinois - Springfield.

and then

and then